Mar 12, 2026

Underwriting is a decision. Lending is a system. Most fintech companies have confused the two, and small businesses are paying for it.

Traditional loan products require regulated infrastructure that takes significant time and engineering effort to build correctly. State-by-state licensing, bank partner coordination, payment rail integration, and audit requirements don't lend themselves to fast iteration. MCAs became the default in early fintech lending because they avoid most of that complexity, and for most SMBs they remain the most accessible form of financing available. The result is that small businesses routinely pay effective APRs exceeding 100% for capital that could be available at a fraction of that cost through a properly structured term loan. The difference isn't underwriting. It's infrastructure.

The industry's obsession with underwriting is understandable. Determining whether to extend credit to a small business is a difficult problem, particularly because financial signals for SMBs are often fragmented across multiple systems and data sources. But operating a regulated SMB lending program requires much more. Systems must move funds, coordinate with banking partners, manage state transitions across multiple parties, and maintain a complete audit trail across the full life of a loaIn embedded SMB lending, these challenges become even more pronounced. Loans originate through partner platforms, which means the entire process, from application through funding and beyond, must operate reliably with minimal manual intervention.

Prime was designed to address both sides of this problem. The platform combines underwriting capabilities with the infrastructure required to operate traditional SMB loan products. This infrastructure allows Prime to offer APR-based financing that can produce significantly lower effective costs for borrowers. Because regulatory frameworks are built directly into the platform, the same infrastructure can support a broader range of lending products over time.

To support this model, the architecture follows three core principles.

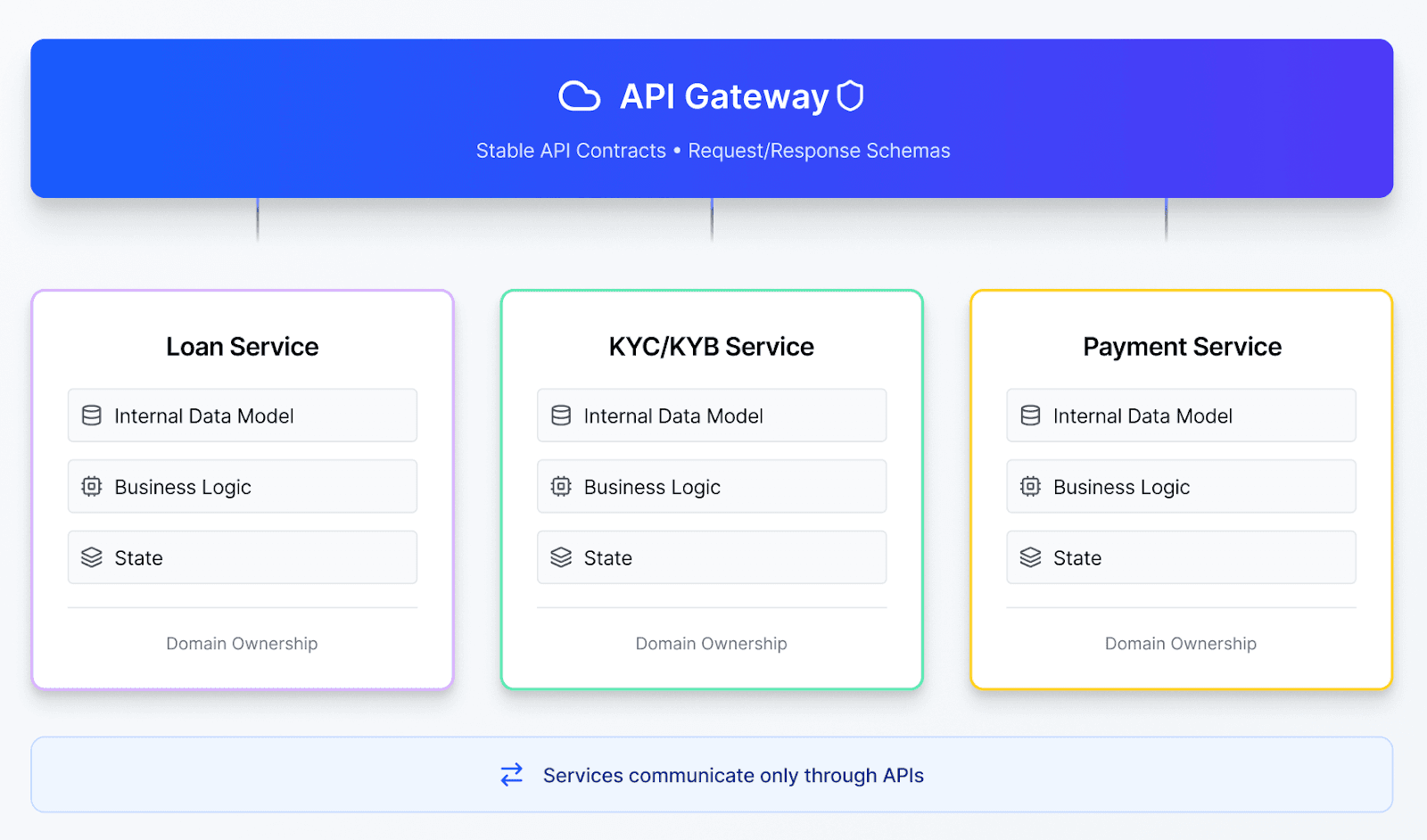

01. Domain-Owned Data Models

Operating SMB loans over time requires managing state across multiple domains. Loans move through stages such as application, approval, funding, and servicing, and each stage interacts with different systems.

Rather than sharing data models across services, our architecture follows a domain-driven approach in which each service owns its internal data model and manages its state independently.

Domain Ownership

Services encapsulate their internal representations of business objects and manage them within the service boundary. These models are not exposed to other services, and callers cannot depend on their structure.

Stable API Contracts

Services communicate through APIs with predefined request and response schemas. Callers may supply external identifiers when creating or referencing objects. This allows their systems to associate their records with the corresponding records maintained by the service.

This design preserves clear ownership of state while maintaining stable integration boundaries between services.

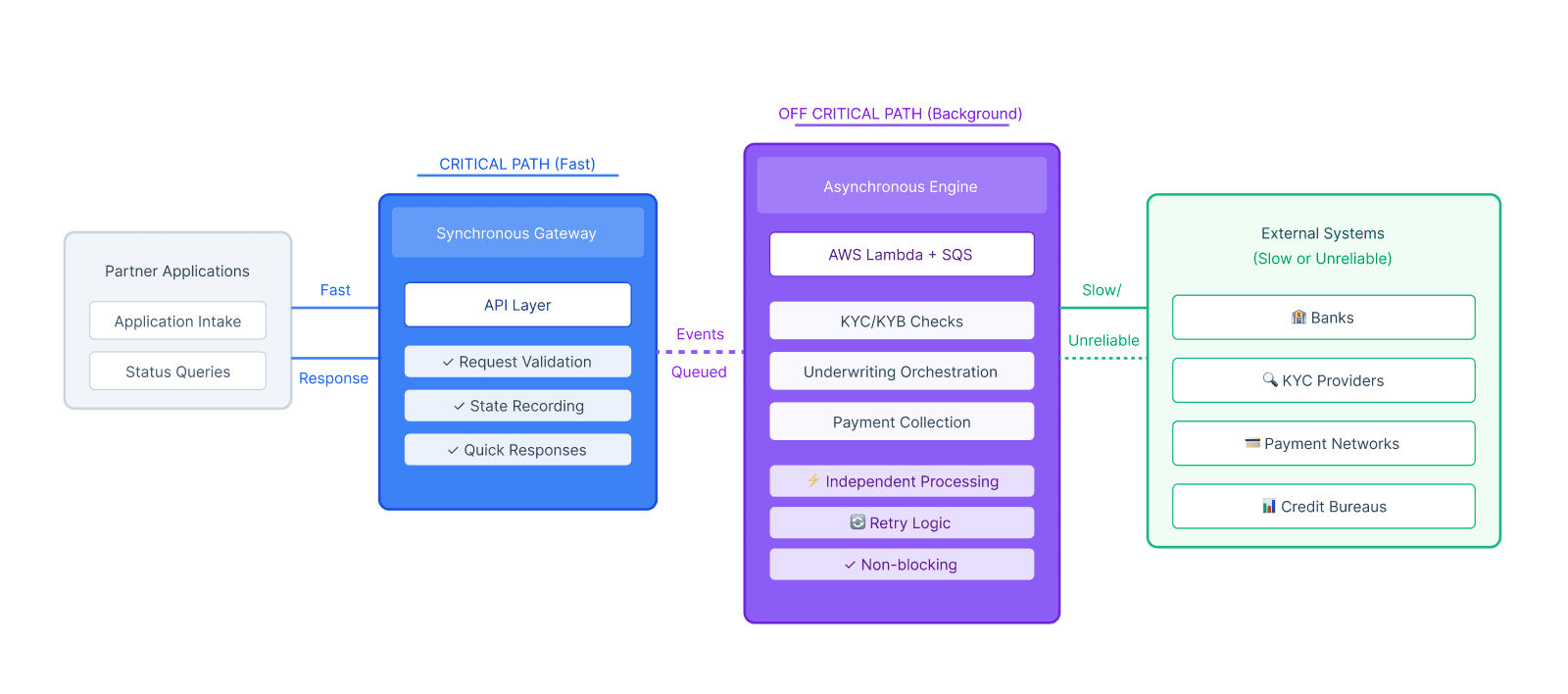

02. Asynchronous Processing for Fast APIs

SMB lending workflows must coordinate with external financial systems while remaining responsive to partner applications.

External systems such as banks, KYC providers, and payment networks can be slow or unreliable. This makes purely real-time processing difficult to scale.

Our approach keeps the API focused on fast interactions while moving latency-prone work off the critical path.

The Synchronous Gateway

The API layer handles partner-facing operations such as application intake and status queries. It validates requests, records state, and returns responses quickly.

The Asynchronous Engine

Operations that depend on external systems, including KYC and KYB checks, underwriting orchestration, and payment collection, run through an event-driven worker system built on AWS Lambda and SQS. Tasks are queued and processed independently. When external services respond slowly or fail, the system retries the work without blocking the API.

This separation keeps partner interactions responsive while allowing lending workflows to progress reliably in the background.

03. Operational Integrity

Financial systems must ensure that every action is consistent, traceable, and auditable.

Prime is designed for operation in regulated financial environments. The architecture emphasizes safeguards that ensure financial operations remain consistent and secure.

Financial operations must execute exactly once and remain fully traceable throughout the lifecycle of the loan.

Atomic Integrity

We use idempotency keys and unique identifiers so requests can be safely retried without duplicating transactions. This protects against network failures, service restarts, and other partial failure scenarios.

Auditability

Every state transition during the loan onboarding process is recorded to provide a complete history of how a loan reached its initial funded state. Subsequent lifecycle events are captured through system integrations that report changes in loan status. Together, these records provide a continuous audit trail across the full lifecycle of the loan.

Institutional Controls

The platform includes role-based access controls, SOC 2 Type II aligned security practices, and comprehensive logging. These controls provide operational oversight while limiting access to sensitive financial operations.

This foundation allows the system to operate reliably at scale while maintaining the traceability required in regulated financial systems.

Solving the SMB Lending Puzzle

Underwriting determines whether credit should be extended to a business. That is a tractable problem with a defined scope.

Operating the systems that move and manage that credit over time is different. The state space is larger, the failure modes are more varied, and the consequences of getting it wrong are financial and regulatory, not just technical.

Building this infrastructure correctly takes time. The compliance frameworks, bank partnerships, payment rail integrations, and audit systems described here represent years of engineering and execution. While operating MCA products provides some foundation, the regulatory obligations, state licensing requirements, loan lifecycle management, and audit trails specific to traditional lending products represent a substantial body of work in their own right. Prime was built to take both problems seriously, and that foundation is what makes reliable, institutional-grade SMB lending at scale possible.

Want to learn more? Click here to schedule a demo.